Understanding the Impact of Inflation on Your Long-Term Savings

nflation quietly erodes the value of your money over time. Learn how it affects your long-term savings — and smart ways to protect your financial future.

11/7/20252 min read

Inflation is often called the “silent thief” — and for good reason. While it doesn’t happen overnight, it gradually reduces the purchasing power of your money, meaning what you can buy today will likely cost more tomorrow.

If you’re saving for retirement, a home, or your children’s education, understanding inflation’s impact is essential to preserving and growing your wealth over time.

What Is Inflation?

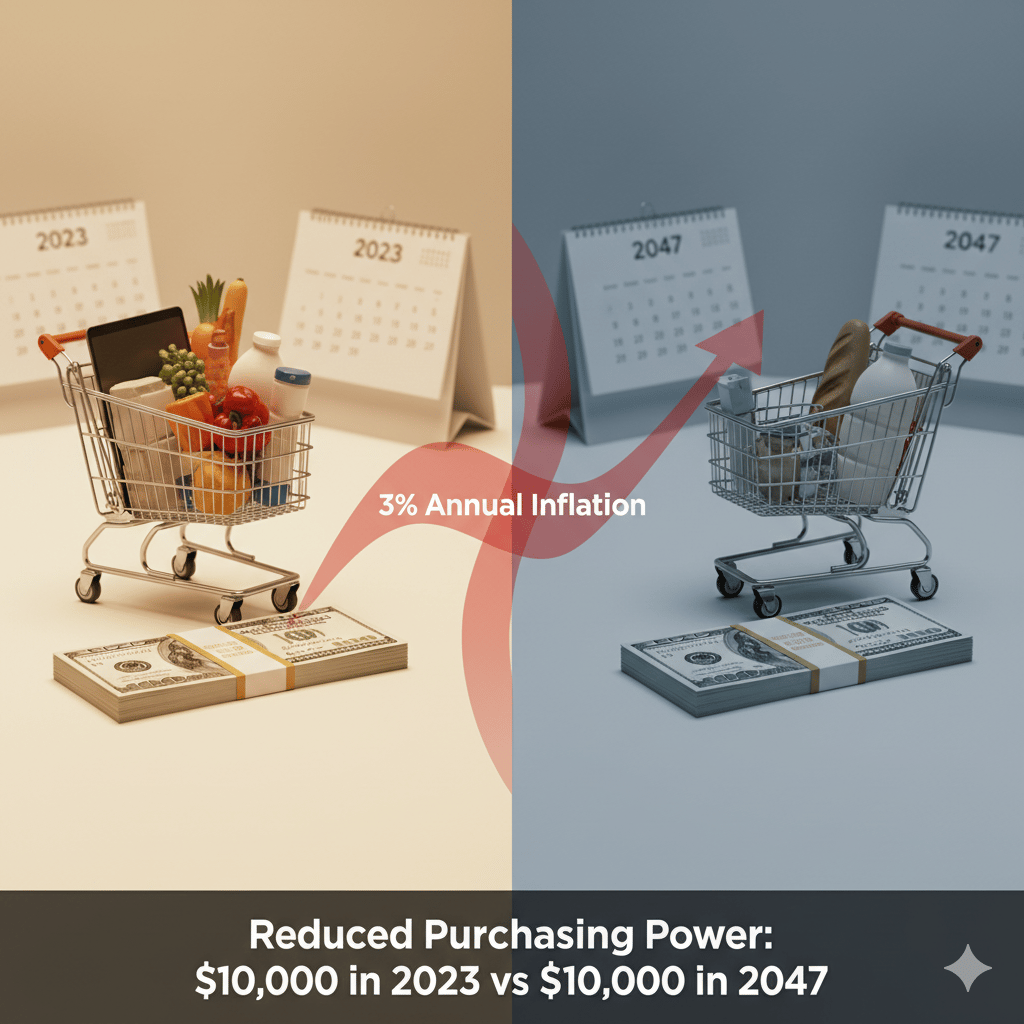

Inflation refers to the general increase in prices of goods and services over time. In Canada, the Bank of Canada aims to keep inflation around 2% per year.

That may sound small, but even moderate inflation can significantly erode your savings in the long run. For example, at 2% inflation, something that costs $1,000 today will cost about $1,220 in 10 years.

The Real Cost of Inflation on Savings

When your savings don’t grow faster than inflation, your real purchasing power decreases. This means that even though the number in your bank account stays the same — its true value declines.

Cash loses value: Money kept in low-interest savings accounts can’t keep up with rising prices.

Fixed-income investments lag behind: GICs or bonds with low returns may not outpace inflation.

Retirement plans fall short: If you don’t account for inflation, your future income might not cover your living expenses.

In short: if your investments don’t grow faster than inflation, you’re actually losing money in real terms.

How to Protect Your Long-Term Savings

1. Invest in Growth Assets

Over the long term, stocks, ETFs, and equity funds have historically outperformed inflation. Even though they carry more short-term risk, they offer higher potential returns that help your money grow in real value.

2. Use Tax-Advantaged Accounts

Make the most of RRSPs and TFSAs. These accounts help your investments grow tax-free or tax-deferred, allowing more of your returns to compound over time — which can offset inflation’s effect.

3. Diversify Your Portfolio

A mix of assets — stocks, bonds, real estate, and inflation-protected investments — provides balance. Consider real assets like real estate or commodities, which often rise in value during inflationary periods.

4. Revisit Your Savings Goals Regularly

Inflation rates change, and so should your strategy. Review your savings targets and investment performance at least once a year to ensure you’re staying ahead of rising costs.

Inflation and Retirement Planning

Retirees are particularly vulnerable to inflation because they often rely on fixed incomes. To combat this:

Keep part of your portfolio in growth-oriented investments even after retirement.

Consider dividend-paying stocks or inflation-adjusted annuities.

Reassess your withdrawal strategy to maintain purchasing power over time.

Final Thoughts

Inflation is inevitable — but losing to it isn’t.

By investing strategically, using tax-efficient accounts, and adjusting your financial plan regularly, you can ensure your long-term savings continue to grow in real value.

Insurance

© 2025 TiKi Wealth. All rights reserved. In partnership with Experior Financial Group Inc. Privacy Policy Terms of Service Disclaimer

Investment

Other

Subscribe to Our Newsletter

Stay updated with the latest financial news and tips.